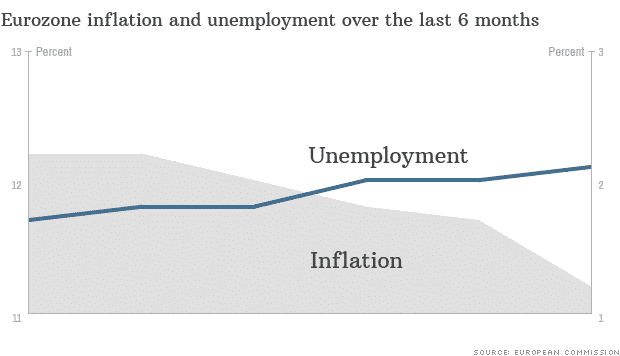

In October 2013 inflation in the Eurozone fell to 0.7%. This is a million miles away from the ECB target of close to but below to 2%. It is clear disinflation territory and uncomfortably close to outright deflation.

In October 2013 inflation in the Eurozone fell to 0.7%. This is a million miles away from the ECB target of close to but below to 2%. It is clear disinflation territory and uncomfortably close to outright deflation.Economic managers and monetary authorities fear deflation much more than inflation. The last thing Europe needs is a Japanese style lost decade of deflation which increases the heavy load of the debt and condemns Europe to eternal shocking levels of unemployment, with all the social problems that this would entail.

Deflation is a spiral. If prices start falling consumptions drops as buying tomorrow will be cheaper than buying today. The downward momentum will build on itself. Breaking the spiral will be as difficult as running uphill just as you are sliding down the slope.

One gets the impression that Europe is in an institutional paralysis, unable to take the necessary measures to address the slide to deflation. Germany and France who ultimately have the final say in the EU are unable to work together to find a real solution. Not just that, but they are also failing in giving the ECB, the only institution that can act with the speed guaranteed by its autonomy, the necessary backing to take extraordinary measures that are justified by these extraordinary circumstances.

Germany is so out of touch with the existential problems of the EU and the Euro that they had to be publicly warned by the US Treasury. Germany has been a net beneficiary of the Euro crisis so much so that the country is now sitting on a Balance of Payments surplus which in nominal terms is bigger than China's and which runs up to some 7% of the GDP. This is disequilibrium at its best. Structural surpluses require adjustment as much as structural deficits and deficits can only be addressed if surpluses are reduced. Simple maths!

But the Germans just do not get it. Rather than give heed to US criticism they deny the obvious by replying:

" The German current account surplus is no cause for concern, neither for Germany, nor for the Eurozone or for the global economy. There are no imbalances in Germany that need correction."

This is quintessential self-denial and delusion. Of course the German structural surplus is a cause for concern. It is particularly a cause for concern to the Euro countries in distress that can only address their deficits if Germany opens up and stimulates domestic demand to reduce its surplus. Otherwise their sacrifices will prove futile. We cannot have all Euro countries in surplus. Attempts to do so challenge the basic laws of mathematics.

But even if Germany were to convert and adopt looser policies which have been demanded by the IMF and now by the US, that would be a long term solution which offers little comfort to the immediate threat of sliding from disinflation to deflation.

This risk needs to be addressed by the instant adoption of much looser monetary accommodation by the ECB. Reducing interest by a further quarter point would be quite irrelevant from a monetary stance but it helps to reduce the exchange value hardness of the Euro to enhance the export competitiveness of the countries performing structural adjustments. But real solution demands additional monetary stimulus beyond the provision of cheap liquidity to EU banks.

Given the difficulty for the ECB to adopt QE on the lines adopted by its counterparts in the US, UK and Japan ( because the ECB, unlike the other Central Banks, does not have a single Treasury that issues the securities of one central government) the ECB has to think further and go beyond QE or OMT, which has so far remained unused as too complicated to adopt.

The ECB has to consider outright monetisation to recapitalise the ESM on a large scale so that the ESM will have the ready resources to fund recapitalisation of European Banks. Not until European Banks are generously recapitalised will they start to honour their true function to oil economic growth with supply of credit to private companies and SME's. And without properly function credit markets periphery economies in the EU will never shake off their distress, especially if Germany continues in denial and insist on their right to enjoy their surpluses.

Europe must act before sliding into dangerous deflation territory.

No comments:

Post a Comment