We the People of the United States, in Order to form a more perfect Union, establish Justice, insure domestic Tranquillity, provide for the common defence, promote the general Welfare, and secure the Blessings of Liberty to ourselves and our Posterity, do ordain and establish this Constitution for the United States of America.

The above is the preamble to the Constitution of the United States.

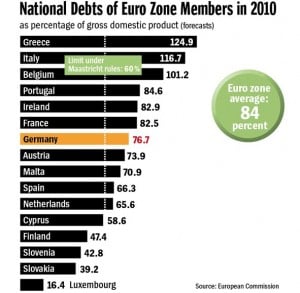

Today I put myself in the shoes of a middle class Greek citizen. A normal Joe Citizen , neither one from the oligarchies who thrived on political patronage and the ensuing corruption, nor one of those who turn democratic protest into distasteful violence and clashes with law and order forces. One from

we the people.

Just think of me as Nikos with responsibility to put food on the family table but can’t see how can I do that. I lost my job, there is small prospect of finding decent work and can only work part-time at a reduced minimum wage in a job which degrades my skills. I have unavoidably fallen behind on my mortgage payments while the Bank is threatening to pull the plug on me.

It's hard time to be Greek these days.

It is no honour to form part of a race that defaults on its obligations, that needs its creditors to write off 70% of what we owe them and be patient for the remaining 30% which we will hope to repay only over 20 years. It is humiliating having foreign creditors dictating to us what we can and cannot do, and forcing us into austerity packages which is crushing our economy, just when we need investments and growth to give us some hope of a tiny light at the end of the tunnel.

I am angry at Greek politicians that promised us heaven and drove us to hell. Hell can't be much worse than what I am going through. But there is something which hurts more than the austerity pain, the insecurity and the humiliation we are going through. It is seeing the two classes of mischief who brought us to hell negotiating behind our back and serving us with round after round of austerity without offering any hope that this will lead to redemption; and all this without giving us any say on the matter.

It hurts to see politicians from the whole spectrum of Greece's political parties, the chief architects of our financial disaster, sitting in Cabinet, always at each other's throat, pretending they are defending our interest and preparing for early elections so they send the technical PM back to where he belongs and they can go back to their old political games. It hurts also to see EU leaders and bureaucrats putting pistol to our politicians’ brains and giving them cover for accepting something they would never accept except at gunpoint. These are the same EU leaders and bureaucrats who let Greece into the Euro knowing fully well we were not ready for it, knowing fully well the risks in blocking the safety valve of having one's own currency to compensate for the lack of competitiveness of the economy, and who turned time and time again more than a blind eye as our politicians cheated and lied their way through the Euro rules.

I know we are sitting between a rock and a hard place. I know that the alternative to the austerity rounds being served upon us is dirty default and probably exit from the Euro and possible also from the EU. This will change our savings, salaries and pensions into worthless drachmas and we will be in hell squared or cubed.

But I demand a choice. I demand to choose between the rock and the hard place.

I demand that the EU appreciates that they are partly responsible for the sad state we are in. I demand that they condition their bailout to Greece having a totally technocrat cabinet, to Greek politicians going to parliament to support the technocrat cabinet with the necessary legislative measures; that a medium term redemption plan is explained to the people so that we can have the opportunity to approve it in a referendum; that based on such referendum our politicians will have to support by legislative measures the plan which the people vote for.

If the people choose to burn in hell squared or cubed than at least it would be our choice. But believe me the Greeks are not the mobs you see on television attacking the police. The Greeks are like me suffering in silence and eagerly awaiting someone offering us a serious long term austerity plan which can be executed by serious technical people who can keep up our realistic hopes for light at the end of the dark tunnel as we go through excruciating pain of fiscal adjustment.

The EU must not trust the politicians that destroyed us to execute the austerity program. They will just ruin us.