_______________________________________________________________________________

If the Economist Business Round Table held in Malta earlier this month served for nothing, it served to raise awareness among international speakers and delegates that Malta is an island of stability representing the best of core Europe in its periphery.

Given the problems encountered by

periphery countries like Greece, Cyprus, Portugal and Ireland (who all had to

seek bailout from the EU) as well as Spain and Italy (who avoided full scale

bailout but have been subjected to strict austerity measures and have seen

their banking sectors seriously impaired by the financial crisis) Malta was often

unfairly grouped with this sickly grouping.

As it so happened practically a couple of days before the Malta Round

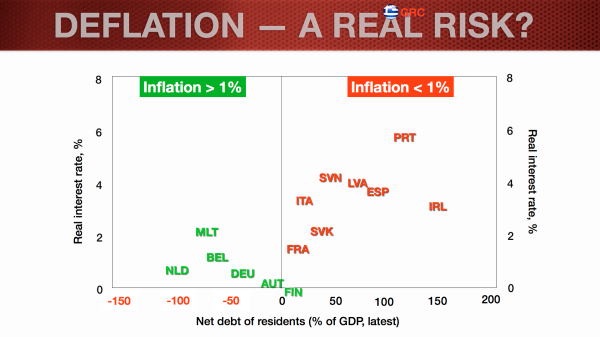

Table the International Monetary Fund (IMF) posted on its web-site an article titled

"Euro

Area: Deflation versus Lowflation". IMF

posted the chart below which shows the countries on the left half of the chart

with an inflation rate higher than 1%. Malta is in this group with the best of

the breed i.e. Finland; Austria; Germany; Belgium and The Netherlands. In the right half there are the countries

experiencing inflation lower than 1% and causing apprehension about the risk of

their flirting with an outright deflationary environment.

Not only Malta is on the virtuous page but we are the country with the

most normal rate of inflation giving a real interest rate of about 2% which all

economic text books would define as having the optimum position often referred

to as Goldilocks economics i.e. not too hot causing high inflation and price

bubbles and not too cold causing risks of stagnation and deflation. Our net

debt as a percentage of GDP is also healthy.

If you should be wondering why having real inflation less than 1% is

bad, it is because very low inflation ( or possibly negative i.e. prices

falling rather than rising) as being experienced in Spain, Italy, Latvia,

Slovenia and Portugal, all on the top right half of the table, means these

countries are suffering high real rate of interest ( i.e. nominal rate adjusted

for inflation/deflation) which scares away investment and keeps down economic

growth. In Malta because we have very

moderate but positive normal inflation, the real rate of interest is lower and this

stimulates investment and economic growth.

During last week’s European Central Bank (ECB) press conference,

President Draghi described the Eurozone as an “island of stability”. If he were referring to Malta he would be

right as we have stable inflation in the context of healthy economy

growth. But calling the whole Eurozone

an “island of stability” may be a bit of a stretch. With Eurozone inflation

well below the 2% target for over a year and projected to stay so until at

least 2017, the Eurozone can aptly be described as the “island of price

stability”. But price stability at a level well below the 2% gives the

stability of the cemetery rather than the stability of economic growth needed

to address chronic unemployment.

Very low inflation may sound like a good thing, but one of the risks of

prolonged low inflation is that it could become entrenched in inflation

expectations and people’s behaviour, thereby becoming the new norm. President

Draghi knows this, but perhaps because the current ECB configuration does not

allow enough room to manoeuvre with symmetry when inflation undershoots as when

it overshoots, the ECB is pretending that low inflation is not a problem.

It definitely

is a problem and the point was made emphatically by

Martin Wolf, chief economic editor of the Financial Times this week in an

article titled "The spectre of eurozone deflation". The main points/quotes

of the article are:

·

ECB should

announce a symmetrical inflation target of 2% indicating it will henceforth

treat excessively low inflation as a problem no less serious than rapidly

rising prices.

·

Ultra low

inflation is dangerous. If inflation in strong core countries is low then

inflation in crisis hit countries must be close to zero or negative.

·

If average

inflation stood at 2% with the surplus countries at say 3% and adjusting

countries at 1% the Eurozone would be in far better shape.

·

ECB should

implement a programme of quantitative easing; negative deposit rates should

also be considered.

·

ECB would

suffer a deep split if it sought to adopt such a policy.

·

The fear

(is) that the ECB may be forced to pretend that low inflation is not a threat because

it cannot agree on what to do about it.

·

ECB might

do little about it (fragile economic recovery of the Eurozone) because the

measures it would need to take are controversial (with the Germans).

·

ECB's job

is to stabilise the Eurozone not the German economy. If the ECB's policy

takes care of the latter rather than the former than the Eurozone is not a

currency union, it is something quite different altogether.

Personally I do not agree that ECB needs to do

something as controversial as quantitative easing or as risky as negative

deposit rates. ECB needs to license the ESM as a bank, give

unlimited liquidity access to the ESM through its discount windows, widen the

eligibility of assets available for discount and force the ESM to use this

liquidity to recapitalise massively fragile banks in periphery Eurozone so that

the banks can start acting as banks and no longer as zombies. In so doing

it would strengthen the transmission mechanism for ECB's monetary

policy. SME's in Italy, Spain, Portugal Ireland and Greece must

find the necessary bank credit support and at a comparative price as much as

SME's anywhere else in the Euro area.

Malta should be proud of being a sample of core Europe in its periphery, but we would be much better off if other countries around us are truly helped by the ECB to heal rather than merely being kept alive by artificially low interest rates.

Malta should be proud of being a sample of core Europe in its periphery, but we would be much better off if other countries around us are truly helped by the ECB to heal rather than merely being kept alive by artificially low interest rates.

No comments:

Post a Comment